Beyond growth: How dividend strategies can unlock returns in Asia

For asset owners seeking income, resilience and long-term exposure to Asia’s dynamic equity landscape, the case for dividend investing is increasingly compelling. Nilang Mehta, Head of Asia Dividend & India Offshore Equity discusses further in this article.

For professional investors and intermediaries only. This document should not be distributed to or relied upon by retail clients/investors.

This article was written in collaboration with AsianInvestor.

For years, equity income was seen as a defensive allocation more naturally associated with global developed markets than with Asia. That perception is shifting.

Amid uncertainty in international markets, strategies focused on Asia income can be considered as a core allocation capable of delivering income, resilience and disciplined exposure to long-term equity growth – not a niche tool for cautious investors.

The renewed case reflects both market conditions and structural change. In a world shaped by higher volatility, geopolitical fragmentation and less predictable interest-rate cycles, investors are placing greater value on stable income streams and more durable return drivers.

“With global uncertainty on the rise, an Asia high-dividend strategy can potentially offer robust growth, attractive yield, and diversification in the search for more reliable income over the longer term,” said Mehta.

A coming of age for dividend investing in Asia

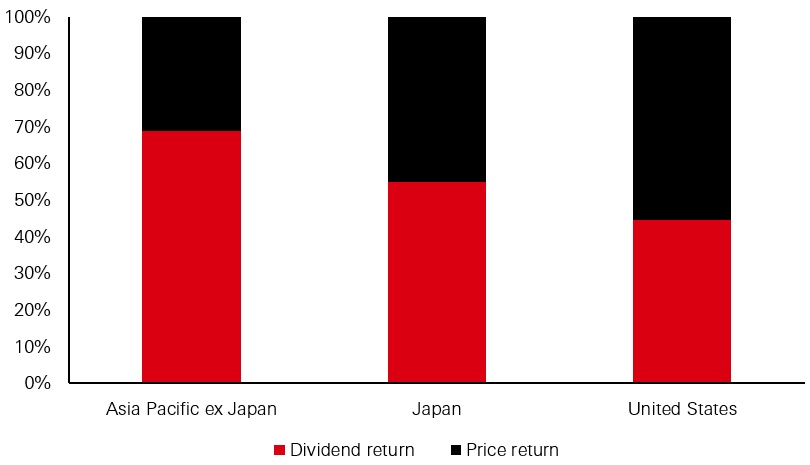

Asian equities are becoming increasingly relevant in that context. As the chart shows, dividends accounted for approximately 69 per cent of total returns in Asia Pacific ex Japan since 2000, versus 45 per cent in the US. At the same time, dividend growth in Asia has the potential to rise faster than developed markets, underpinned by strong free cash flows.

Total return contributions since 2000

Dividend and price returns as a percentage of total return

Source: HSBC Asset Management, Bloomberg, as of 31 March 2026

MSCI country indices are used to represent the equity performance of the indicated markets.

Past performance does not predict future returns. For illustrative purpose only.

However, this has often been overshadowed by Asia’s reputation as a pure growth story. That narrative still holds, but the opportunity set is broader. Given the region’s diversity, spanning developed and developing markets, there is a wider and differentiated universe of companies – from established dividend payers with strong free cash flow, to cyclical leaders in sectors like energy and materials, to growth-oriented firms which are increasingly combining reinvestment with rising capital returns.

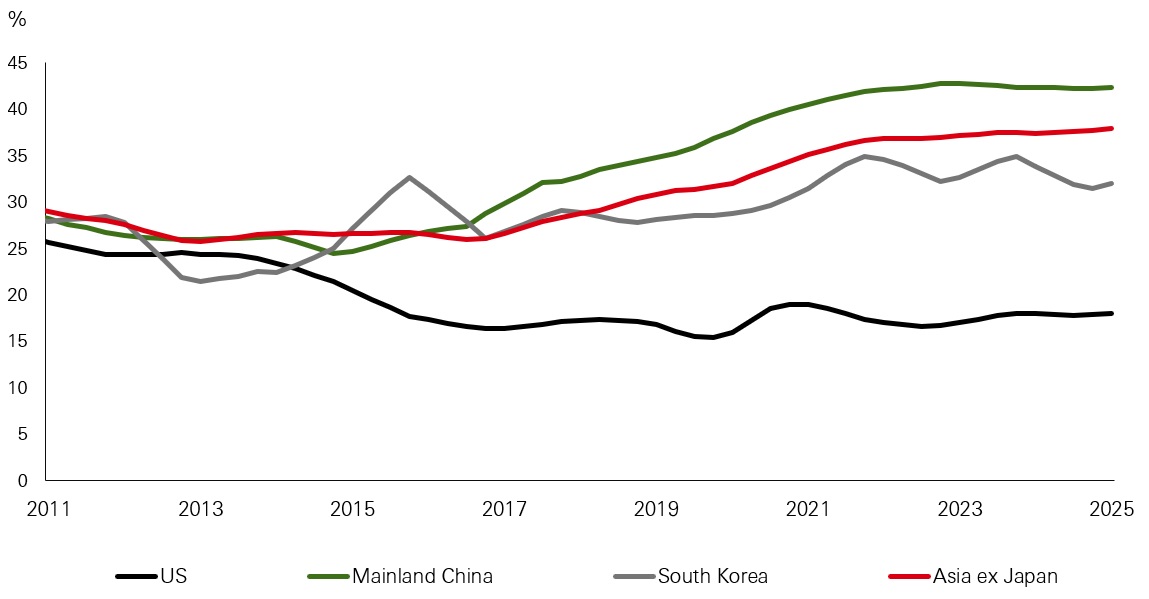

Further, Asia’s share of mature cash-generative businesses reinforces the region’s corporate balance sheets. On average, Asian companies hold significantly higher net cash levels than their counterparts in Europe and the US, providing greater flexibility to sustain and grow shareholder distributions over time. This financial strength creates scope for rising payout ratios, special dividends and buybacks – particularly as governance standards and capital allocation frameworks continue to evolve across the region.

Percentage of companies which are net cash positive

Source: FTSE, HSBC Global Research, as of 31 December 2025

Past performance does not predict future returns. For illustrative purpose only.

“For asset owners seeking a more balanced way to access Asia, dividend investing offers a combination of quality bias and participation in structural growth,” Mehta said.

Dividend strategies often demonstrate their strength during more challenging market environments. While they may underperform during periods of rapid growth or market exuberance, they have the potential to deliver stronger risk-adjusted returns over the full market cycle by minimising losses during downturns and offering a steady stream of income. In this way, dividend investing can be seen as a balanced strategy – not necessarily leading in every phase, but likely to endure across diverse market conditions.

Asia is well suited to this approach. Investors can access relatively stable income from mature sectors in markets such as Australia, Singapore and Korea, while capturing dividend growth from companies in faster-growing economies such as India and parts of Mainland China.

Korea: reforms driving a shift in shareholder returns

Structural changes are reinforcing this opportunity. Across Asia, dividend investing is entering a new phase. Policy shifts, changing investor needs and improving governance standards, supported by rising institutional ownership, greater scrutiny and the influence of global capital, are driving a stronger focus on shareholder returns across the region.

South Korea offers one of the clearest examples of this shift. Historically, Korean equities have traded at a persistent valuation discount, explained Mehta, reflecting low payout ratios, weak governance perceptions and a greater focus on majority shareholders.

The government’s Corporate Value-Up programme aims to address these issues by encouraging better capital allocation, stronger disclosure and higher shareholder returns.

For investors, the significance lies in both reform momentum and starting point. Korean payout ratios have historically been low, leaving considerable room for growth. Combined with improving governance and strong earnings potential in sectors such as technology, this creates scope for a multi-year expansion in dividends and buybacks.

Mainland China: income in a lower-yield market

Mainland China presents a different but equally relevant income case.

There is growing interest in equities with stable dividend characteristics, particularly in high-yielding sectors such as banks and energy. These companies can offer mid-single-digit yields, often supported by strong balance sheets, defensive earnings profiles and, in some cases, policy backing.

Policymakers have also encouraged dividends and buybacks as a way to support market confidence, alongside a broader push to strengthen corporate governance standards. These initiatives potentially pave the way for more consistent, transparent and shareholder-aligned capital return policies over time.

For long-term investors, Mainland Chinese dividend payers can serve as equity-income proxies – offering steady cash generation alongside potential for capital appreciation.

Within a regional portfolio, Mainland China can complement markets such as Korea, said Mehta, by providing stable yield driven by a different set of policy and valuation dynamics.

Securing sustainable dividends

Capturing this opportunity requires a disciplined approach. Simply targeting the highest yields can lead to concentration risk or exposure to companies with unsustainable payouts.

“High headline income can sometimes hide weak fundamentals, excessive leverage, or structural decline, making it critical to avoid these ‘dividend traps’,” said Mehta. “An effective strategy focuses on income quality rather than income alone, with an emphasis on strong balance sheets, robust free cash flow and credible capital allocation to drive sustainable and reliable returns.”

Driving income-driven, diversified returns

Against this backdrop, active management plays a central role. This is also important for a regional income strategy such as HSBC’s Asia Pacific ex-Japan equity high dividend approach, which is not simply about maximising yield – it is about constructing a diversified risk-adjusted return profile that blends income with capital growth.

The strategy is built on three complementary pillars: defensive companies that provide steady income through reliable cash flows and consistent capital returns; cyclical companies poised to benefit from improving economic or sector conditions, driving dividend growth through rising earnings; and growth companies with strong financials that balance expansion with increasing shareholder returns.

This three-fold approach broadens the opportunity set beyond traditional high-yield stocks. It allows the strategy to capture multiple sources of return while remaining disciplined on quality and sustainability.

It also supports more effective risk management by balancing current yield with future growth and by avoiding concentrations in any single sector or style.

Ultimately, in a world of unsynchronised monetary cycles, uncertain investment outcomes and recurring geopolitical shocks, dividend strategies offer a practical way to remain invested in Asia without relying solely on capital appreciation.

The views expressed above were held at the time of preparation and are subject to change without notice. The value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested. The level of yield is not guaranteed and may rise or fall in the future.

Key risks

The value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested.

- Exchange rate risk: Investing in assets denominated in a currency other than that of the investor’s own currency perspective exposes the value of the investment to exchange rate fluctuations

- Concentration risk: Funds with a narrow or concentrated investment strategy may experience higher risk and return fluctuations and lower liquidity than funds with a broader portfolio

- Emerging market risk: Emerging economies typically exhibit higher levels of investment risk. Markets are not always well regulated or efficient and investments can be affected by reduced liquidity

- Derivative risk: The value of derivative contracts is dependent upon the performance of an underlying asset. A small movement in the value of the underlying can cause a large movement in the value of the derivative. Unlike exchange traded derivatives, over-the-counter (OTC) derivatives have credit risk associated with the counterparty or institution facilitating the trade

- Operational risk: The main risks are related to systems and process failures. Investment processes are overseen by independent risk functions which are subject to independent audit and supervised by regulators

- Counterparty risk: The possibility that the counterparty to a transaction may be unwilling or unable to meet its obligations

- Liquidity risk: Liquidity of securities may also fluctuate, resulting in situations where an investor may not be able to buy or sell the security in a timely manner at their preferred price range if the turnover volume were to drop significantly

- Taxation risk: Investors should note that the proceeds from the sale of securities in some markets or the receipt of any dividends or other income may be or may become subject to tax, levies, duties or other fees or charges imposed by the authorities in that market

- Custody risk: Investors should be aware that they are exposed to the risk of the custodian not being able to fully meet its obligation to restitute in a short time frame all of the assets of the Fund in the case of bankruptcy of the custodian

- Sustainable investment policy risk: Sustainable Criteria are subjective and are subject to the Investment Adviser’s discretion. The use of Sustainable Criteria may affect the Fund’s investment performance

- Sustainability risk: Sustainability risk means an environmental, social or governance event or condition that, if it occurs, could cause an actual or a potential material negative impact on the value of the investment.

Important Information

For Professional Clients and intermediaries within countries and territories set out below; and for Institutional Investors and Financial Advisors in the US. This document should not be distributed to or relied upon by Retail clients/investors.

The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested. The performance figures contained in this document relate to past performance, which should not be seen as an indication of future returns. Future returns will depend, inter alia, on market conditions, investment manager’s skill, risk level and fees. Where overseas investments are held the rate of currency exchange may cause the value of such investments to go down as well as up. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in emerging markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries and territories with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries and territories in which they trade.

The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings. The material contained in this document is for general information purposes only and does not constitute advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We do not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The views and opinions expressed herein are those of HSBC Asset Management at the time of preparation and are subject to change at any time. These views may not necessarily indicate current portfolios' composition. Individual portfolios managed by HSBC Asset Management primarily reflect individual clients' objectives, risk preferences, time horizon, and market liquidity. Foreign and emerging markets: investments in foreign markets involve risks such as currency rate fluctuations, potential differences in accounting and taxation policies, as well as possible political, economic, and market risks. These risks are heightened for investments in emerging markets which are also subject to greater illiquidity and volatility than developed foreign markets. This commentary is for information purposes only. It is a marketing communication and does not constitute investment advice or a recommendation to any reader of this content to buy or sell investments nor should it be regarded as investment research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination. This document is not contractually binding nor are we required to provide this to you by any legislative provision.

All data from HSBC Asset Management unless otherwise specified. Any third-party information has been obtained from sources we believe to be reliable, but which we have not independently verified.

HSBC Asset Management is the brand name for the asset management business of HSBC Group, which includes the investment activities that may be provided through our local regulated entities. HSBC Asset Management is a group of companies in many countries and territories throughout the world that are engaged in investment advisory and fund management activities, which are ultimately owned by HSBC Holdings Plc. (HSBC Group).

- In Australia, this document is issued by HSBC Bank Australia Limited ABN 48 006 434 162, AFSL 232595, for HSBC Global Asset Management (Hong Kong) Limited ARBN 132 834 149 and HSBC Global Asset Management (UK) Limited ARBN 633 929 718. This document is for institutional investors only and is not available for distribution to retail clients (as defined under the Corporations Act). HSBC Global Asset Management (Hong Kong) Limited and HSBC Global Asset Management (UK) Limited are exempt from the requirement to hold an Australian financial services license under the Corporations Act in respect of the financial services they provide. HSBC Global Asset Management (Hong Kong) Limited is regulated by the Securities and Futures Commission of Hong Kong under the Hong Kong laws, which differ from Australian laws. HSBC Global Asset Management (UK) Limited is regulated by the Financial Conduct Authority of the United Kingdom and, for the avoidance of doubt, includes the Financial Services Authority of the United Kingdom as it was previously known before 1 April 2013, under the laws of the United Kingdom, which differ from Australian laws;

- In Bermuda, this document is issued by HSBC Global Asset Management (Bermuda) Limited, of 37 Front Street, Hamilton, Bermuda which is licensed to conduct investment business by the Bermuda Monetary Authority;

- In France, Belgium, Netherlands, Luxembourg, Portugal, Greece, Finland, Norway, Denmark, Spain and Sweden this document is issued by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026);

- In Germany, this document is issued by HSBC Global Asset Management (Deutschland) GmbH which is regulated by BaFin (German clients) respective by the Austrian Financial Market Supervision FMA (Austrian clients);

- In Hong Kong, this document is issued by HSBC Global Asset Management (Hong Kong) Limited, which is regulated by the Securities and Futures Commission. This content has not been reviewed by the Securities and Futures Commission;

- In India, this document is issued by HSBC Asset Management (India) Pvt Ltd. which is regulated by the Securities and Exchange Board of India;

- In Italy, this document is issued by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026), through its Italian branch, regulated by Banca d’Italia and Commissione Nazionale per le Società e la Borsa (Consob);

- In Japan, this document is issued by HSBC Asset Management (Japan) Ltd (JRN 3010001124868), regulated by the Financial Services Agency;

- In Malta, this document is issued by HSBC Global Asset Management (Malta) Limited which is regulated and licensed to conduct Investment Services by the Malta Financial Services Authority under the Investment Services Act;

- In Mexico, this document is issued by HSBC Global Asset Management (Mexico), SA de CV, Sociedad Operadora de Fondos de Inversión, Grupo Financiero HSBC which is regulated by Comisión Nacional Bancaria y de Valores;

- In the United Arab Emirates, this document is issued by HSBC Investment Funds (Luxembourg) S.A. – Dubai Branch (Level 20, HSBC Tower, PO Box 66, Downtown Dubai, United Arab Emirates) regulated by the Capital Market Authority (CMA) in the UAE to conduct investment fund management, portfolios management, fund administration activities (CMA Category 2 license No.20200000336) and promotion activities (CMA Category 5 license No.20200000327).

- In the United Arab Emirates, this document is issued by HSBC Global Asset Management MENA, a unit within HSBC Bank Middle East Limited, U.A.E Branch, PO Box 66 Dubai, UAE, regulated by the Central Bank of the U.A.E. and the Capital Market Authority in the UAE under CMA license number 602004 for the purpose of this promotion and lead regulated by the Dubai Financial Services Authority. HSBC Bank Middle East Limited is a member of the HSBC Group and HSBC Global Asset Management MENA are marketing the relevant product only in a sub-distributing capacity on a principal-to-principal basis. HSBC Global Asset Management MENA may not be licensed under the laws of the recipient’s country of residence and therefore may not be subject to supervision of the local regulator in the recipient’s country of residence. One of more of the products and services of the manufacturer may not have been approved by or registered with the local regulator and the assets may be booked outside of the recipient’s country of residence.

- In Singapore, this document is issued by HSBC Global Asset Management (Singapore) Limited, which is regulated by the Monetary Authority of Singapore. The content in the document/video has not been reviewed by the Monetary Authority of Singapore;

- In Switzerland, this document is issued by HSBC Global Asset Management (Switzerland) AG. This document is intended for professional investor use only. For opting in and opting out according to FinSA, please refer to our website; if you wish to change your client categorization, please inform us. HSBC Global Asset Management (Switzerland) AG having its registered office at Gartenstrasse 26, PO Box, CH-8002 Zurich has a licence as an asset manager of collective investment schemes and as a representative of foreign collective investment schemes. Disputes regarding legal claims between the Client and HSBC Global Asset Management (Switzerland) AG can be settled by an ombudsman in mediation proceedings. HSBC Global Asset Management (Switzerland) AG is affiliated to the ombudsman FINOS having its registered address at Talstrasse 20, 8001 Zurich. There are general risks associated with financial instruments, please refer to the Swiss Banking Association (“SBA”) Brochure “Risks Involved in Trading in Financial Instruments”;

- In Taiwan, this document is issued by HSBC Global Asset Management (Taiwan) Limited which is regulated by the Financial Supervisory Commission R.O.C. (Taiwan);

- In Turkiye, this document is issued by HSBC Asset Management A.S. Turkiye (AMTU) which is regulated by Capital Markets Board of Turkiye. Any information here is not intended to distribute in any jurisdiction where AMTU does not have a right to. Any views here should not be perceived as investment advice, product/service offer and/or promise of income. Information given here might not be suitable for all investors and investors should be giving their own independent decisions. The investment information, comments and advice given herein are not part of investment advice activity. Investment advice services are provided by authorized institutions to persons and entities privately by considering their risk and return preferences, whereas the comments and advice included herein are of a general nature. Therefore, they may not fit your financial situation and risk and return preferences. For this reason, making an investment decision only by relying on the information given herein may not give rise to results that fit your expectations.

- In the UK, this document is issued by HSBC Global Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority;

- In the US, this document is issued by HSBC Securities (USA) Inc., an HSBC broker dealer registered in the US with the Securities and Exchange Commission under the Securities Exchange Act of 1934. HSBC Securities (USA) Inc. is also a member of NYSE/FINRA/SIPC. HSBC Securities (USA) Inc. is not authorized by or registered with any other non-US regulatory authority. The contents of this document are confidential and may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose without prior written permission.

- In Chile, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Chilean inspections or regulations and are not covered by warranty of the Chilean state. Obtain information about the state guarantee to deposits at your bank or on www.cmfchile.cl;

- In Colombia, HSBC Bank USA NA has an authorized representative by the Superintendencia Financiera de Colombia (SFC) whereby its activities conform to the General Legal Financial System. SFC has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Colombia and is not for public distribution;

- In Costa Rica, the Fund and any other products or services referenced in this document are not registered with the Superintendencia General de Valores (“SUGEVAL”) and no regulator or government authority has reviewed this document, or the merits of the products and services referenced herein. This document is directed at and intended for institutional investors only.

- In Peru, HSBC Bank USA NA has an authorized representative by the Superintendencia de Banca y Seguros in Perú whereby its activities conform to the General Legal Financial System - Law No. 26702. Funds have not been registered before the Superintendencia del Mercado de Valores (SMV) and are being placed by means of a private offer. SMV has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Perú and is not for public distribution;

- In Uruguay, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Uruguayan inspections or regulations and are not covered by warranty of the Uruguayan state. Further information may be obtained about the state guarantee to deposits at your bank or on www.bcu.gub.uy.

Copyright © HSBC Global Asset Management Limited 2026. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of HSBC Asset Management.